Delay Social Security to Supercharge Your Roth Conversions?

Delaying Social Security isn't just about a bigger check — for retirees with large pre-tax balances, it's often about buying more Roth conversion runway. Here's how deferring to 70 keeps your MAGI low, neutralizes the tax torpedo, and lets you convert more aggressively before the window closes.

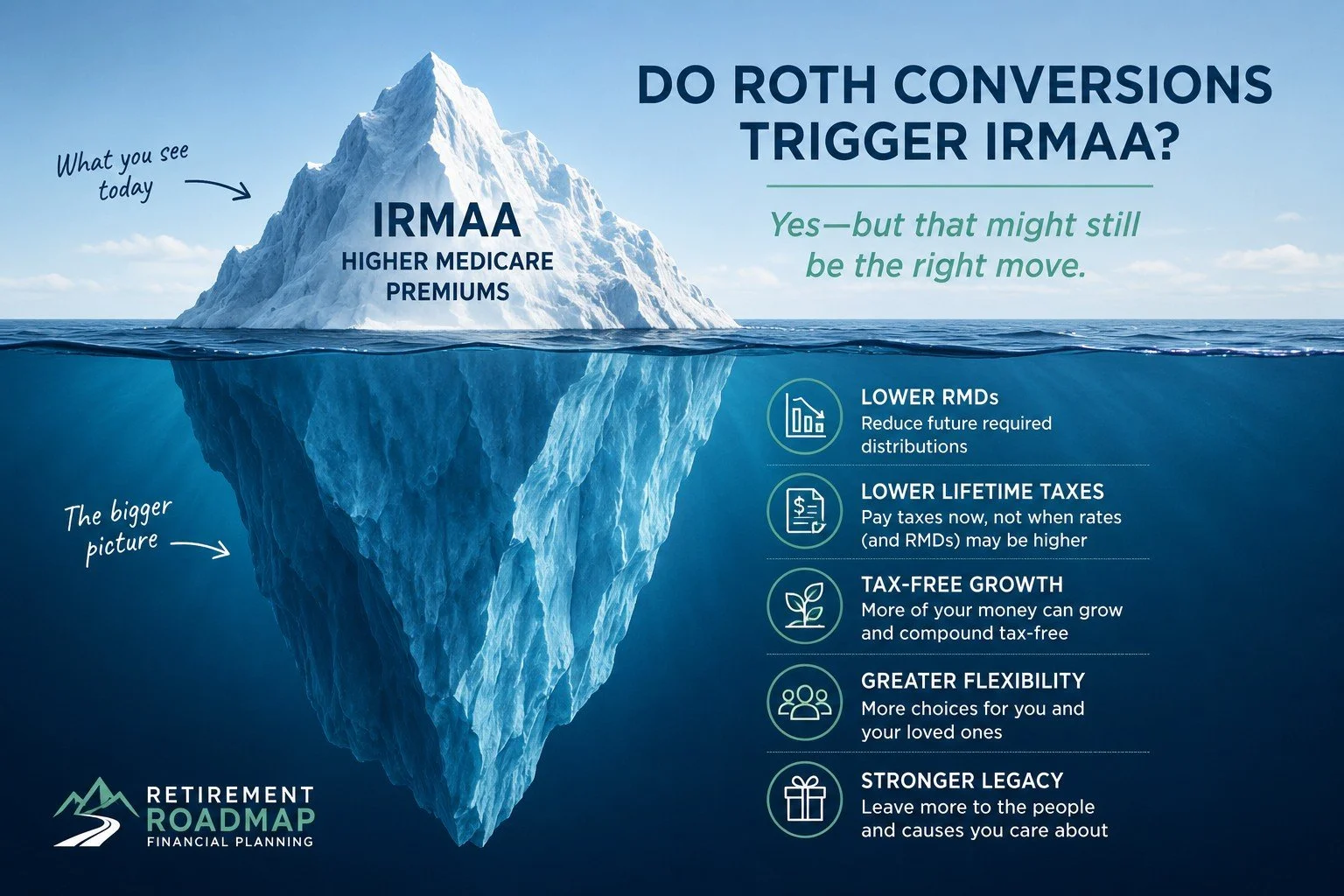

Do Roth Conversions Increase Medicare Premiums?

Yes — but the more important question is whether that changes anything. A Roth conversion can trigger an IRMAA surcharge on your Medicare premiums two years later. Here's what it costs, when it's still worth doing, and how to model it into your strategy.

Managing RMDs Before They Manage You

Required Minimum Distributions can quietly push retirees into higher tax brackets, increase Medicare premiums, and reduce long-term flexibility. Learn strategies to proactively manage RMDs before they start managing your retirement.

Roth Conversions: Don’t Set It and Forget It

A Roth conversion strategy isn't a light switch you flip once. Tax law, your health, your partner's life, charitable goals, and where you live can all shift the math — here's what to revisit every year.

How Much Should You Convert to Roth Each Year?

There's no universal Roth conversion number. But there is a logical process for finding yours — one that looks at tax brackets, Medicare premiums, and what you're actually trying to accomplish. Get the 2026 numbers and a step-by-step framework.

The Widow's Tax Problem — and Why Roth Conversions Are Often the Answer

Most couples don't realize that losing a spouse doesn't just mean losing a partner — it means losing access to joint tax brackets, often overnight. The result is higher taxes on the same income, for the rest of your life. Here's how Roth conversions can change that math before it's too late.

The Roth Conversion That Wasn’t Worth It

If you plan to give to charity, Roth conversions may not be as powerful as advertised. Here's how QCDs can reduce your RMDs and taxes more effectively — and why the sequence matters.

Roth Conversion Strategies for Retirement Planning

Roth conversions can reduce lifetime taxes when used strategically. Learn when they make sense, when they don’t, and how they interact with Social Security, Medicare, and required minimum distributions.